Key takeaways

- Class 4 NIC for 2025/26 is 6% on profits between £12,570 and £50,270, then 2% above, following the cut from 8% that took effect in April 2024.

- Class 2 NIC remains at £3.45 per week on a voluntary basis for self-employed workers who wish to protect state pension entitlement despite the April 2024 abolition.

- The personal allowance stays frozen at £12,570 and the higher rate threshold at £50,270, meaning more self-employed earners are pulled into higher tax bands by wage growth.

- Making Tax Digital for Income Tax starts 6 April 2026 for sole traders and landlords with gross income above £50,000, requiring quarterly digital record submissions.

- The dividend allowance dropped to £500 from April 2024, down from £1,000 the previous year, increasing the tax bill for self-employed owner-managers taking dividends.

Self-employment tax changes to 2022/23

Here's a summary of the self-employment tax changes for 2022/23. This includes new UK tax brackets, updates to thresholds and rates introduced in the Spring Statement.

1. What is the personal allowance for 2022/23?

The rate at which people start paying national insurance(which will take effect from July) will be £12,570 – the same as the income tax personal allowance.

However, the planned 1.25% increase in national insurance contributions must remain a "dedicated funding source" for health and social care.

What does this mean for you?

In the long run, if your earnings rise and the personal allowance (the amount you do not have to pay tax on) stays the same, you'll pay more in tax.

UK tax brackets 2022/23 for self-employed.

The income tax rates and thresholds for the self-employed in 2022/23 are the same as in 2021/22. The rates are as follows:

● Basic rate – 20% on income between £12,571 and £50,270 – you pay tax on£37,700

● Higher rate – 40% on income between £50,271 and £150,000

● Additional rate– 45% on income above £150,000

2. By how much has National Insurance Increased?

In light of the coronavirus and its impact on the UK economy, the Government intends to raise the National Insurance Tax rate by 1.25% temporarily. After a certain period, this will be replaced by the Health and Social Care Levy of 1.25% in 2023.

If you're self-employed

You need to pay both Class 2and Class 4 National Insurance through your annual Self Assessment tax return if you're self-employed.

If you own a small business

If you're a small businessowner with staff, you also need to pay employees National Insurance contributions via payroll.

Earnings below the Small profits threshold incur no National Insurance Contributions (NICs), but class 2 NICs can be paid voluntarily.

Here are the National Insurance rates:

● Class2 NICs at £3.15 per week

● Class4 NICs up to the upper profits limit at 10.25%

● Class4 NICs above the upper profits limit at 3.25%

Class1 Employer and employee National Insurance contributions.

If you're an employer or have income from employment, here are the Class 1 National Insurance tax thresholds.

%2520National%2520Insurance.jpeg)

Earnings above the primary threshold obtain National Insurance Contributions at 13.25% in 2022/23.

Earnings above the upper earnings limit obtain National Insurance Contributions at 3.25%in 2022/23.

Tax thresholds for Class 1 (secondary) National Insurance.

Employer NICs are due on annual salary payments to employees above a certain threshold, set at £9,100 in2022/23 (a weekly threshold of £175); an increase from £8,840 in 2021/22.

The rate is 15.05 per cent in2022/23 (up from 13.8 per cent in 2021/22).

National Insurance is also due at this rate on any work benefits you give employees. You can find more information here regarding this subject matter for all classes.

You can find more information here regarding this subject matter for all classes.

3. What are the changes in wage rates for employers?

The government has set a national minimum wage and a national living wage to guarantee the lowest paid workers get a minimum standard of pay. This is a legal requirement for all businesses of any size. In April the Chancellor announced an increase across all the rates, with variations based on age group and for apprentices.

4. What are the tax rates for dividends in 2022/23?

Dividend tax rates and National Insurance will increase by 1.25% to pay for the Government's coronavirus response costs.

The dividend allowance(amount of dividends you're not taxed on) remains £2,000. Past that, here are the rates:

● Basic rate taxpayers – 8.75% (up from 7.5%)

● Higher rate taxpayers – 33.75% (up from 32.5%)

● Additional rate taxpayers – 39.35% (up from 38.1%)

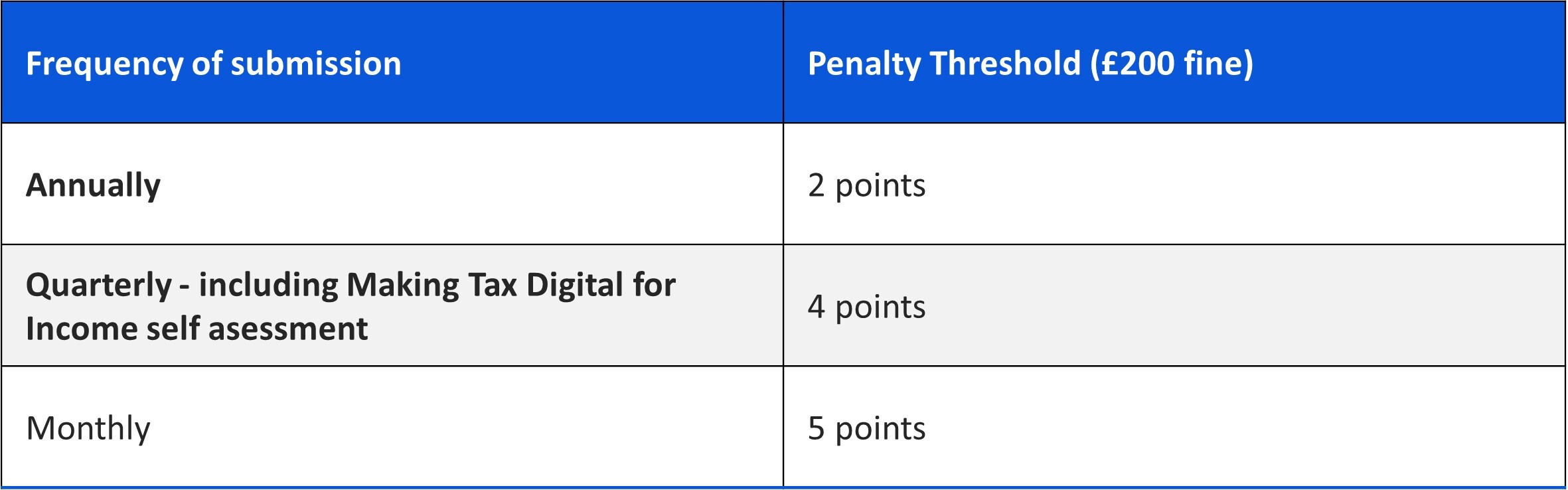

5. When are the points-based tax penalties coming into effect?

The new tax penalty essentially punishes those who are late in paying taxes. How the system works is that you'll get a penalty point for missing a deadline rather than an automatic fine. Therefore, the more deadlines missed, the more points obtained. Taxpayers will face a fine of £200when they reach a certain number of points and another fine for every subsequently missed deadline. The change is due to start in January 2023.

In April, the new penalties were supposed to launch for VAT alongside Making Tax Digital's rollout to all VAT-registered businesses, but HMRC's systems won't be ready in time.

6. What is the new plastic packaging tax introduced for 2022?

If your business manufactures or imports plastic packaging as part of your business, you may be subject to the new plastic packaging tax, which will take effect from April 2022.

According to gov.uk, it applies "if you've manufactured or imported ten or more tonnes of finished plastic packaging components within the last 12 months, or will do so in the next 30 days."

If you meet either of those thresholds, it is advised you register for the tax.

For further information, visit: 'https://www.gov.uk/government/publications/introduction-of-plastic-packaging-tax-from-april-2022/introduction-of-plastic-packaging-tax-2021'

7. Business rates discount.

Businesses in the retail, hospitality and leisure industries face the prospect of getting a 50% discount (previously 66 per cent) of up to £110,000 on their business rates. Furthermore, the increase in business rate multipliers has been put on hold for the 2022/2023 year. This discount should be administered automatically by local authorities.

8. Optimum Directors Salary 2022/23.

The optimum director's salary in 2022/23 is now £11,908 per annum due to the change in the National Insurance (NI) rate.

The lower earnings limit for NI in 2022/23 is £6,396 per annum. It will count as a qualifying year for your future state pension if you earn over this amount.

The primary earnings limit for NI in 2022/23 is £11,908 per annum. If your annual salary exceeds this amount, the employee will need to pay NI contributions.

The secondary earnings limit for NI in 2022/23 is £9,100 per annum (£758 per month). If your annual salary exceeds this amount, the employer (your business)will need to pay NI contributions. A £758 per month salary maximises the corporation tax relief as well as there being a contributory state pension for a year provided by the Government without paying for PAYE or National Insurance

The optimum in 2022/23 is a salary of precisely£11,908, which ensures the taxpayer qualifies for the state pension but does not need to pay any employee contributions. You can qualify for a state pension without making any personal NI contributions. If you're the sole director and pay yourself a salary through your own limited company, the best amount to pay is £9,100 per annum (or £758.33 a month).

● It's at the secondary threshold, so your company won't need to pay the employer's National Insurance on it.

● This salary is lower than the primary threshold, so you won't need to pay an employee's National Insurance.

● It's above the Lower Earnings Limit, so you will still earn National Insurance credits, which is excellent news for your state pension.

● This is less than the tax-free Personal Allowance threshold.

● A sole director cannot claim the Employment Allowance.

Having two or more directors on the company payroll means that you're eligible to claim the Employment Allowance. In 2022/23, the primary threshold will increase mid-year.

You will start paying employees' NI at £9,880 until July 2022, when the threshold increases to £12,570.

In 2022/2023, the optimum salary in a company with two or more directors is £11,908. Two or more directors can take an annual salary up to the primary threshold without paying an employee's NI and then claim the £5,000 Employment Allowance to cover the portion of the employer's NI they would otherwise obtain. If you have another source of income(s), the director's payroll becomes PAYE payroll and is subject to tax and NI as usual, as the actual payroll took up the personal allowance of £12,570.

Main points and other UK tax brackets 2022.

● The Capital Gains Tax allowance remains £12,300 for individuals and£6,150 for trusts, with the rates remaining the same too

● Corporation Tax remains at 19 per cent, but it will be higher for larger businesses in2023

● Other allowances remain the same, including the Individual Savings Account (ISA) allowance at £20,000, the dividend tax allowance at £2,000, and no changes to tax on savings interest

● As announced in the Spring Statement, fuel duty has been cut by 5p a litre

● The Employment Allowance increases from£4,000 to £5,000