Introduction

Welcome to GoForma, your trusted source for clear and practical insights into the best business bank accounts in the UK. Choosing the right business bank account plays a big role in how smoothly your business runs. In this guide, we break down the essentials of business banking and compare three leading options: Tide, Revolut, and Metro, so you can pick the one that fits your business needs.

We road-tested these business bank accounts so you do not have to.

We started with three contenders that stand out on features and costs on paper. We then put them through real-world testing, looking closely at usability, ease of sign-up, response times and the day-to-day banking experience.

You will find the full details below, giving you a clear view of what each account feels like from the inside, without the hassle of opening multiple accounts yourself.

We also used independent data from BVA BDRC, a well-known consumer insight consultancy. They regularly run a large-scale survey for the Competition and Markets Authority (CMA) to measure how likely business customers are to recommend their bank. Around 20,600 small business banking customers were surveyed across 17 banks. We have used this data to support the comparisons in this article.

It’s a long read, so let’s start with the conclusion and summary for those who want to see the results first.

Tide vs Metro vs Revolut - Which is Best?

Different businesses have different needs, so there is no single business bank account that suits everyone.

Freelancers and contractors usually want something quick to set up and easy to run day to day. In that case, Tide works well thanks to its fast onboarding and simple app. It also offers a sign-up incentive of £50 plus free company registration, which makes it a strong starting point.

If you prefer a more traditional setup and value face-to-face support, Metro Bank is a solid choice. Its physical branches and in-person service still appeal to many business owners.

For small businesses that need powerful features, international payments and app-based tools, Revolut stands out as the strongest option.

Tide offers a good sign up incentive of £50 + Free Company Registration for which you can apply here.

Summary: the winner depends on your needs

Every freelancer, contractor and small business needs a business bank account.

The issue is that many people simply choose the bank their accountant suggests or stick with the same high street bank they use personally. They often stay there even when the service falls short.

Spending time upfront to choose the right business bank account can:

save you hassle during the sign-up process, which is often slow and frustrating

give you a better banking experience over the life of your business

support your wider financial goals, such as making international payments, setting up direct debits, or applying for a mortgage in the future

In short, the best business bank account depends entirely on what you need from it.

| Criteria | Revolut | Metro Bank | Tide |

|---|---|---|---|

| Perks on paper | 1st | 2nd | 3rd |

| Sign-up experience | 1st | 3rd | 2nd |

| Day-to-day banking | 1st | 3rd | 1st |

| Customer service | 3rd | 2nd | 3rd |

| Overall recommendation | 1st for small businesses | 3rd | 2nd for freelancers and contractors |

Understanding a Business Bank Account

What is a Business Bank Account?

A business bank account is designed to manage business finances and keep them separate from personal spending. It helps sole traders, partnerships and limited companies handle payments, track income and expenses, and keep a clear view of their business finances.

If you set up a limited company in the UK, the law requires you to open a business bank account. If you are self-employed, a business account is not mandatory, but it makes it much easier to separate business transactions from your personal money.

Business Account vs. Personal Account

Understanding the difference between a business account and a personal account helps you choose the right setup for your finances.

| Aspect | Business Account | Personal Account |

|---|---|---|

| Purpose | Built for business transactions and operations | Used for personal finances |

| Legal structure | Supports sole traders, partnerships and limited companies | Owned and used by one individual |

| Transaction volume | Handles a high volume of payments and receipts | Usually lower transaction levels |

| Fees and charges | May include business-specific fees | Standard personal banking fees |

| Account name | Shows the business name | Shows the individual’s name |

| Access for others | Allows multiple authorised users | Usually limited to the account holder |

| Account features | Invoicing, merchant services and business tools | Budgeting, savings and personal tools |

| Tax reporting | Keeps business and personal tax records separate | Supports personal tax reporting |

| Additional features | Business managers, online tools and integrations | Personal money management features |

Key Features of Business Bank Accounts

- Transaction processing

Business accounts support a high number of transactions, which helps you manage cash flow efficiently. - Multiple payment channels

You can send and receive money through online banking, mobile apps and card or merchant services. - Account management tools

Business accounts offer tools to track transactions and monitor finances in real time. - Business loans and credit

Many accounts give access to overdrafts, credit lines or business loans when needed. - Accounting software integration

Integration with accounting software helps with record keeping and accurate financial reporting.

Who Needs a Business Bank Account?

1. Business owners and entrepreneurs

All types of business owners benefit from a business bank account. It keeps personal and business finances separate and simplifies accounting.

2. Start-ups and small businesses

Start-ups and small businesses use business accounts to track expenses, manage cash flow and build credibility with investors and lenders.

3. Established enterprises

Growing businesses rely on business accounts to manage payroll, supplier payments and more complex financial activity.

4. Contractors and freelancers

Contractors and freelancers use business accounts to receive payments, manage expenses and issue invoices professionally.

Why do You Need a Business Bank Account?

1. Legal compliance

For limited companies, a business bank account is a legal requirement. Mixing personal and business finances can lead to compliance issues.

2. Professionalism and credibility

A business account presents a professional image to clients, suppliers and partners.

3. Simplified accounting

Separate accounts make bookkeeping, tax returns and financial reporting far easier.

4. Better tax management

You can clearly identify allowable expenses and report income accurately.

Factors to Consider When Choosing the Best Bank Account for Your Business

1. Understand your business needs

Think about transaction volume, international payments, lending needs and must-have features.

2. Account type and features

Compare business current accounts, savings accounts and merchant services. Look at cards, apps, overdrafts and ATM access.

3. Fees and charges

Review monthly fees, transaction costs, ATM charges and other service fees.

4. Bank reputation and reliability

Check reviews and feedback from other business owners.

5. Local accessibility

If you value face-to-face support, consider branch and ATM availability.

6. Integration with financial tools

Choose a bank that works smoothly with accounting and finance software such as FreeAgent, QuickBooks, Xero.

7. Customer support

Fast response times and knowledgeable support matter when issues arise.

8. Interest rates and overdrafts

If you hold cash in the account, interest rates and overdraft terms can make a difference.

9. FSCS protection

Check whether your deposits are protected under the Financial Services Compensation Scheme. Eligible deposits up to £120,000 are protected if the bank fails.

10. Terms and conditions

Read the small print, including withdrawal limits, penalties and account restrictions.

Documents Required to Open Business Bank Account

Most banks ask for:

- Proof of identity

- Personal address proof

- Registered business address

- Estimated annual turnover

- Companies House formation documents and company number

- Tax return status and VAT number (if registered)

- Number of employees

Some banks may ask for extra documents to confirm credit and banking history.

How to Open a Business Bank Account?

Opening a business bank account usually follows these steps:

- Check your eligibility

- Complete the application online or in branch

- Submit the required documents

- Wait for approval and receive your account details and debit card

Switching Business Bank Accounts

The Current Account Switch Service (CASS) makes switching business bank accounts simple. It is free to use and moves your payments, direct debits and credits to your new bank within 7 working days, backed by the Current Account Switch Guarantee.

Why have I Written this Article?

I wrote this article after being pushed towards high street banks more than once and feeling let down by the service every time.

I first started contracting in 2015. At the time, I did not even realise I needed a business bank account until my accountant pointed it out. He advised me to open an account with HSBC, saying it would be quicker than waiting two weeks with my personal bank, NatWest. He also claimed he could speed things up thanks to a contact at a local branch.

I trusted his advice. I visited the branch, sat through a 90-minute account opening meeting and walked away thinking the hard part was over.

It wasn’t.

HSBC turned out to be a poor choice. The online banking system and mobile app felt clunky and outdated. Getting hold of support by phone took far too long whenever an issue came up. When I stopped contracting a few months later, I closed the account without hesitation.

In 2017, I returned to contracting and once again needed a business bank account quickly for an upcoming role. My new accountant suggested Santander or Metro Bank. After explaining my previous experience, he recommended Santander and told me I could apply online without visiting a branch.

Santander was a clear step up from HSBC. The account opening process felt smoother and the online interface worked better. That experience alone showed me why comparing business bank accounts matters.

That said, it still was not great. The mobile app felt dated and, after 18 months, I started paying £7.50 per month in fees. It was acceptable, but nothing more. I did not dislike it, but I did not rate it either.

As challenger banks became more popular, I felt there had to be better options. I already used Monzo for my personal banking and liked how simple and user-friendly it was. That pushed me to look deeper into digital-first business banks.

I started researching challenger banks properly, and I am very glad I did.

High Street vs Challenger Bank

I focused my search on business bank accounts offered by challenger banks only.

Why?

After spending hours comparing high street business accounts with challenger options, I found that traditional banks rarely offer anything extra beyond a physical branch network. Even then, that advantage is not exclusive. Metro Bank combines digital banking with physical branches, which removes one of the main reasons people stick with high street banks.

Based on this, I narrowed my shortlist to three challenger banks that offer a strong mix of features for business users: Metro Bank, Revolut and Tide.

Metro Bank offers a physical branch network, while Revolut and Tide operate as online-only platforms. I also looked at Aldermore, which pays interest on business deposits. However, due to consistently poor reviews on Trustpilot, I decided not to include it in this comparison.

Selecting the Best Business Bank Account - Criteria

I wanted to take a practical and hands-on approach when comparing business bank accounts. To do this, I opened business accounts with each of the shortlisted banks and assessed them based on real usage rather than marketing claims.

I used a four-point scoring process focused on what actually matters to business owners.

These were the key areas I assessed:

- Features vs cost on paper

Including monthly fees, international payments, cash deposits, account types and FSCS protection. - Sign-up process

How easy and fast it is to open a business bank account. - Day-to-day banking

The quality of online banking, mobile apps and general usability. - Customer service and support

How easy it is to get help and how responsive the support teams are.

This approach helped highlight which business bank accounts perform well in real-world use, not just on paper.

The Details and the Experience

1. Features vs Cost (on Paper)

On paper, the three business bank accounts on this shortlist serve very different needs.

Metro Bank stands out for its physical presence, with branches across the UK. That said, its digital and online banking tools feel more limited when compared to digital-first challengers.

Tide focuses on freelancers, contractors and small businesses that want fast onboarding and practical tools such as invoicing and team cards.

Revolut is clearly built with small businesses in mind, especially those that need advanced features, international payments and deep software integrations.

Let’s break down why each account performs the way it does.

Winner (for freelancers and contractors): Tide

For freelancers and contractors, Tide offers the best balance of speed, simplicity and business-friendly tools.

Tide makes it quick to open a business bank account and provides a clean app and desktop experience. It also includes features that are genuinely useful for solo business owners, such as invoicing, expense categorisation and the ability to issue cards to team members if needed.

Here’s where Tide performs well:

- Fast and simple sign-up

You can open an account quickly without visiting a branch. - Useful business features

Invoicing tools and team cards work particularly well for freelancers and contractors. - Accounting software integrations

Tide integrates with Xero, FreeAgent and Sage, which suits most UK contractors and sole traders.

There are trade-offs to be aware of:

- Limited international payments: Tide mainly supports GBP and EUR. Sending or receiving other currencies can be difficult, which makes it less suitable for businesses that trade globally.

- Transaction costs: The free plan charges for outgoing bank transfers, usually around 20p per payment. Paid plans come with monthly fees for added features or extra cards.

- Customer support: Standard support is provided by email. Faster or dedicated support is only available on paid plans such as Tide Pro.

Overall, Tide delivers strong value for freelancers and contractors who prioritise speed, ease of use and practical tools over branch access.

Metro Bank in comparison

Metro Bank’s biggest advantage is its physical branch network. If you regularly deposit cash or prefer face-to-face support, this is where Metro Bank wins.

However, this comes at a cost:

- Transaction fees apply for transfers

- A monthly maintenance fee applies unless you keep a minimum balance

- Online and mobile banking feel less intuitive than digital-first challengers

Metro Bank does provide FSCS protection, which adds peace of mind, but its feature set feels more traditional.

Winner (for small businesses): Revolut

Revolut is built for small businesses that need powerful tools rather than basic banking.

Its pricing reflects this. Entry-level plans start with a monthly fee, and higher-tier plans become expensive quickly. While Revolut does offer free accounts, they come with limited functionality before transaction fees kick in.

Where Revolut really stands out is in its advanced features:

Expense management for teams

- Issue prepaid cards to multiple employees

- Allow staff to submit expenses for approval

- Track spending through a central dashboard

Multi-currency and international payments

- Hold and manage multiple currencies in one account

- Exchange and transfer money internationally at competitive rates

- Support employees who spend abroad using business cards

Powerful integrations

- Accounting software such as Xero and FreeAgent

- Workflow tools like Zapier

- An API for businesses that want custom integrations

These features make Revolut ideal for growing businesses, teams with international exposure and owners who want to automate workflows.

2. Sign-up Process

Time matters, especially when you start or restart contracting.

Each time I began contracting, I had only a short window between securing a contract and starting work. That meant moving fast. I needed to set up a limited company, register it with Companies House, find a contractor accountant, arrange a business insurance and open a business bank account.

I wanted a quick, fully online sign-up without branch visits, follow-ups or delays. Challenger banks promise speed, but the reality varies.

Winner: Revolut

Revolut had the smoothest and fastest sign-up process by far.

I opened the account directly through their website. The process involved filling in business details, completing security checks, selecting a pricing plan and making a small initial transfer. While Revolut asked for more information than Tide, everything felt structured and clear.

Once completed, the account opened immediately.

I was initially told the business card would take up to two weeks to arrive, which felt slow by modern standards. In reality, it arrived within five days. The card itself looks premium and well designed, even if it feels lighter than some metal cards on the market.

Revolut also does a great job with onboarding. Their email sequence clearly explains features and helps you get value from the account straight away.

2nd place: Tide

Tide offers a mostly smooth sign-up experience, though it is not instant.

After downloading the app and starting the application, I noticed a few usability issues. Some fields felt clunky, and selecting business details was not as intuitive as it should be. These are small issues, but for an app-only platform, they do affect confidence.

That said, I completed the application in around ten minutes, passed the security checks and submitted everything without needing to visit a branch. Tide advised that approval could take anywhere between five minutes and 48 hours.

In my case, it took the full 48 hours, which felt frustrating at the time. However, given what came later with other banks, Tide’s process still felt reasonable.

A few days later, the Tide card arrived by post. The card design is basic and mine arrived slightly scratched, but these are minor points. Functionally, the account worked as expected.

3rd place: Metro Bank

If speed and convenience matter, Metro Bank sits firmly at the bottom of the list.

To open an account, I had to visit a branch in person. When I called ahead, I was told I could not book an appointment and should allow up to two hours for the process. I also needed to bring multiple documents to prove my address.

After waiting to be seen, the application began. About 30 minutes in, I was told my address had been flagged during a CIFAS check. This was not due to anything I had done, but because someone else in my postcode had attempted fraud in the past.

I was told additional checks were required and that if I passed, I would need to return to the branch and start again. When I asked how often people fail this check, I was told more than half do.

After passing the checks, I returned to the branch only to find that none of my previous details had been saved. I had to answer the same questions again. I made it clear the account needed to be opened within an hour, and the staff member did their best to rush the process.

Even then, the account still needed approval.

A few days later, I received confirmation that the account had been opened. My debit card and a separate letter containing a security word arrived by post. Setting up online banking required a customer number that had not been shared, which meant another call to support.

Eventually, I gained access, but the entire process felt slow, outdated and unnecessarily complex.

3. Day to Day Banking

1st place: Tie between Revolut and Tide

When it comes to everyday banking, both Revolut and Tide perform extremely well.

They offer clean interfaces, intuitive navigation and modern banking tools that make daily tasks quick and painless. Each has its own strengths, which come down to how and where you prefer to manage your finances.

Below is a closer look at each provider.

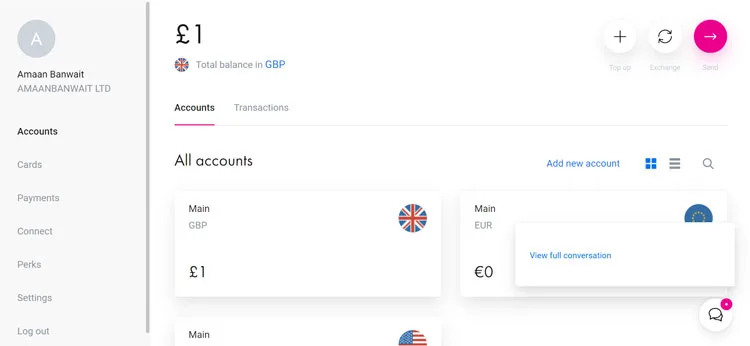

Revolut

Revolut clearly encourages users to manage their account through its desktop platform, and that makes sense. It offers a wide range of advanced features that benefit from a larger screen.

The interface is clean and easy to understand from the start.

Managing cards, creating virtual cards and moving money between currencies feels straightforward. Transferring funds between GBP and EUR accounts works smoothly for both business and personal use.

Revolut’s expense management tools are a real strength. Businesses with employees can issue cards, track spending and manage expenses centrally. Employees can spend abroad without mixing personal and business costs, which removes a lot of friction.

By integrating expense management directly into banking, Revolut removes the need for separate tools and creates a more joined-up experience for growing businesses.

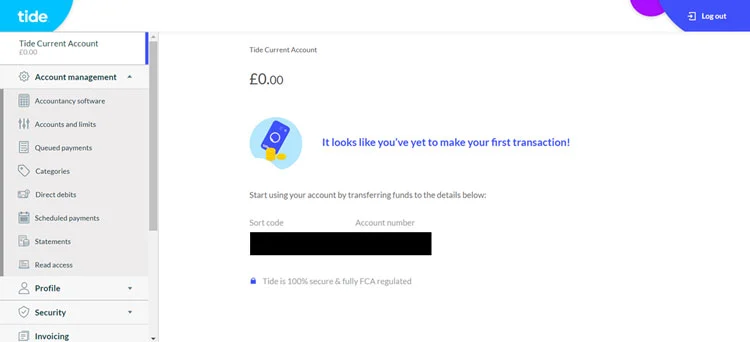

Tide

Tide offers both a mobile app and a desktop platform, and both are well designed.

The app feels clean, fast and very intuitive. In fact, it is one of the easiest banking apps to get comfortable with. The desktop version is equally strong, with a simple menu structure that keeps all key features in one place rather than hiding them behind layers of navigation.

Tide also includes built-in invoicing. Setting up invoices is quick and simple, but the feature does have limits. It works well for basic billing, but it lacks flexibility for more detailed invoicing, such as charging by day rates, quantities or handling multiple currency calculations in a single invoice.

One limitation with Tide is that it does not offer personal bank accounts. While this is not a deal breaker, it does mean you cannot view personal and business finances together in one place.

3rd place: Metro Bank

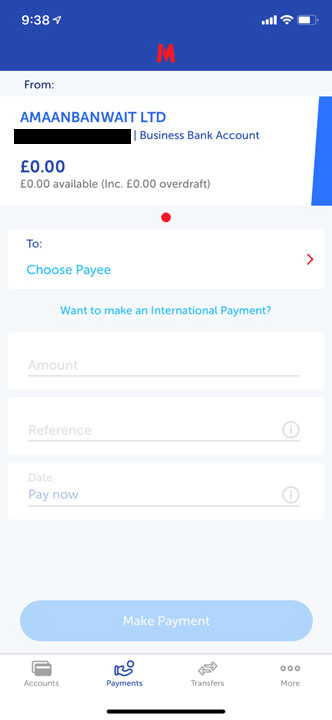

Metro Bank delivers a more traditional banking experience.

Its desktop platform feels closer to a high street bank than a digital-first challenger. While it is more usable than some older banks, simple tasks like making payments require more steps than they should.

The mobile app is noticeably better. It is clean and easy to use, even if it lacks the modern design and polish of Revolut or Tide.

One positive is that Metro Bank allows you to view personal and business accounts within the same app, which many users will appreciate. Combined with its physical branches, this creates a hybrid experience that suits business owners who want digital access alongside in-person support.

Overall verdict on day-to-day banking

For everyday use, Revolut and Tide lead the way thanks to their modern interfaces and efficient workflows. Metro Bank performs well enough, but its digital experience still feels more traditional.

If day-to-day usability matters most, digital-first challengers clearly have the edge.

4. Customer Service

Customer service is a critical part of business banking. If your account is frozen or you need urgent help, you want quick access to a real person who can fix the issue without delays. I looked closely at response times, support channels, and overall experience.

1st place: Metro Bank

Metro Bank performs best for customer service. It offers 24/7 phone support and response times are excellent. On two different occasions I called, one during UK business hours and one outside, I reached a human almost instantly.

Its physical branch network is another advantage, especially for businesses that still value face-to-face banking. That said, my in-branch experience was inconsistent. Follow-ups were slow, some emails went unanswered, and service quality varied between staff members.

Even with those issues, fast phone access and round-the-clock availability give Metro Bank a clear edge overall.

2nd place: Revolut

Revolut’s customer service is entirely chat-based, with no phone support at all. This puts pressure on live chat to perform well, which it currently does not.

In my testing, a simple query took over one hour to receive a response. That delay is hard to accept for a business account, especially when there is no phone option as a backup.

From conversations with other business users, slow response times appear to be a common issue rather than an isolated case.

3rd place: Tide

Tide offers the weakest customer service experience of the three. Phone support is only available for lost or stolen cards, with most queries pushed to email or in-app chat.

Email responses took just over an hour, which is acceptable but far from ideal. Live chat was significantly worse, with waits of more than two hours for basic questions.

For business owners who value quick problem resolution, this lack of responsive support is a serious downside.

Overall Verdict

Metro Bank stands out for customer service thanks to fast, 24/7 phone support. Revolut and Tide lag behind due to slow response times and limited support channels, which can be frustrating for time-sensitive business issues.

Choose the Best Business Bank Account with GoForma

Choosing the right business bank account depends on your priorities as a business owner.

- Metro Bank is ideal if you value fast phone support, physical branches, and a more traditional banking experience.

- Revolut works best for small businesses that need advanced features like multi-currency payments, expense management, and app-based power tools.

- Tide is perfect for freelancers, sole traders, and small businesses that want a simple, intuitive interface and quick sign-up, though FSCS protection is not available.

Each bank has strengths and drawbacks, so consider your business size, daily banking needs, and how much support you want before deciding.

At GoForma, we help you compare options like Tide, Revolut, and Metro Bank and guide you to the best choice for your business.

Book a Free Consultation today and let our expert contractor accountants help you set up the right business bank account and manage your finances with confidence.