What is VAT Registration

If you are planning to start a business in the UK or are already running one, it is essential to understand the Value Added Tax (VAT). VAT is a tax that is levied on goods and services in the UK. In this guide, we will provide you with all the information you need to know about VAT Registration in the UK.

VAT registration involves registering your business with the government to show it's activeness in making and selling goods or services and to collect and pay Value Added Tax (VAT). Once registered, a business is legally required to charge VAT on their sales, known as output tax, and can reclaim VAT on their business-related purchases, known as input tax. You will also need to:

- Charge VAT on any goods or services you sell (and make sure you charge the correct amount!)

- Pay any VAT you owe to HMRC

- Submit VAT Returns

- Keep VAT records and maintain a VAT account

Here I have come up with the complete VAT registration guide to follow

If you are planning to start a business in the UK or are already running one, it is essential to understand the Value Added Tax (VAT). VAT is a tax that is levied on goods and services in the UK. In this guide, we will provide you with all the information you need to know about VAT Registration in the UK.

VAT registration involves registering your business with the government to show it's activeness in making and selling goods or services and to collect and pay Value Added Tax (VAT). Once registered, a business is legally required to charge VAT on their sales, known as output tax, and can reclaim VAT on their business-related purchases, known as input tax. You will also need to:

- Charge VAT on any goods or services you sell (and make sure you charge the correct amount!)

- Pay any VAT you owe to HMRC

- Submit VAT Returns

- Keep VAT records and maintain a VAT account

Here I have come up with the complete VAT registration guide to follow

When to Register for VAT?

Not all businesses are legally required to pay VAT.

You will have no legal obligation to pay VAT if your turnover is below a certain threshold.

Mandatory VAT Registration

register for VAT if:

- Your VAT taxable turnover exceeds the VAT threshold 2024 of £90,000. The VAT taxable turnover refers to the total value of everything you sell that isn't exempt from VAT.

- You expect your UK VAT taxable turnover to exceed £90,000 in the next 30-day period

- Your business had a taxable turnover over £90,000 over the last 12 months

- If you take over a VAT-registered business

You must register for VAT within 30 days of fulfilling these conditions. You can register for VAT online through the UK government's website. You will need to create an account and fill out the online registration form.

Voluntary VAT Registration

Even if your business’s turnover is below the £90,000 VAT threshold, you might choose to register for VAT voluntarily to:

- reclaim VAT on goods and services you buy for your business

- make your business appear more established and credible to customers and suppliers, especially in B2B transactions.

- save the hassle of having to adjust your pricing and accounting systems on exceeding VAT threshold later

Watch below video from HMRC to find out more about registering for VAT:

Exceptions and Special Cases VAT Registration

You must register, regardless of your VAT taxable turnover, if all the following conditions apply:

- You are based outside the UK.

- Your business operates from outside the UK.

- You supply goods or services to the UK or plan to do so in the next 30 days.

- You sell through online marketplaces like Amazon and eBay

If you fail to register on time, you'll need to pay what you owe from the date the registration should have been effective. HMRC may also impose a penalty depending on the amount you owe, how late your registration is and other situational factors.

What is the VAT Threshold?

The VAT registration threshold 2024 is £90,000. This means that businesses with a taxable turnover exceeding £90,000 in either the past 12 months (up to the end of a given calendar month) or in the next 30-day period alone are required to register for VAT with HMRC and charge VAT on their sales. Taxable turnover, sometimes referred to as VATable or VAT taxable turnover, includes sales that are subject to the standard, reduced, or zero rates of VAT. Taxable turnover specifically refers to taxable sales with a UK place of supply. It is important to note that income exempt from UK VAT or with a non-UK place of supply does not count towards the VAT registration turnover threshold.

Documents Required for UK VAT Registration

When applying for VAT registration in the UK, you will need to provide certain documents and information. Here are the key documents typically required:

If you are registering for VAT as a Limited Company:

- your company registration number

- your business bank account details

- your Unique Taxpayer Reference (UTR)

- details of your annual turnover

- your Self Assessment

- your Corporation Tax

- Pay As You Earn (PAYE)

If you are registering for VAT as as an individual or as a partnership:

- your National Insurance number

- an identity document, like a passport or driving license

- your bank account details

- your Unique Taxpayer Reference (UTR), if you have one

- details of your annual turnover

- your Self Assessment return

- payslips

- P60

It's important to note that the specific document requirements may vary based on the nature of your business and individual circumstances. It's recommended to seek professional advice from a small business accountant to ensure you have all the necessary documents for a smooth VAT registration process.

Our Ultimate VAT guide walks through step by step what you need to know about registering for VAT, how to pay your VAT, your filing responsibilities and how to de-register for VAT.

- What is VAT

- When to register for VAT

- VAT rates

- Exempt/ Out of Scope VAT items

- VAT filing responsibilities

- De-registering for VAT

Steps to Register for VAT

- Step 1: Check if you need to register

- Step 2: Gather information

- Step 3: Choose a VAT accounting scheme

- Step 4: Register

- Step 5: Wait for confirmation

Step 1: Check if You Need to Register:

If your business has a taxable turnover of over £90,000 in the last 12 months or is expected to exceed this threshold in the next 30 days, you need to register for VAT.

Step 2: Gather Information:

You will need to provide basic information about your business, such as its legal name, address, and date of incorporation. You will also need to provide information about your business activities and the types of goods or services you sell.

Step 3: Choose a VAT Accounting Scheme:

You will need to choose a VAT accounting scheme, such as standard accounting, cash accounting, or the flat rate scheme. Each scheme has its own benefits and limitations, so it's important to research and choose the one that works best for your business.

Step 4: Register for VAT:

You can register for VAT online through the UK government's website. You will need to create a Government Gateway account if you don't already have one, and then fill out the online VAT registration form. Make sure to provide accurate and complete information to avoid delays or errors. You can also explore other ways to register if you can't register online.

Watch below video from HMRC on how to fill in taxable turnover and business activities on the VAT registration form:

Step 5: Wait for Confirmation:

Once you have submitted your VAT registration form, HMRC will review your application and contact you within a few weeks to confirm your registration. If your application is successful, you will receive a VAT registration number and instructions on how to submit VAT returns.

This is how a VAT registration number looks like on a VAT certificate:

Advantages of VAT Registration

- Legitimacy and Professionalism: Registering for VAT gives your business an added level of credibility and professionalism, as it signals that your company has reached a certain turnover threshold and is operating on a larger scale. This can enhance your reputation with customers, suppliers, and potential business partners.

- Ability to Reclaim VAT: VAT-registered businesses can reclaim the VAT they have paid on eligible business purchases. This includes goods, services, and equipment used for business purposes. Reclaiming VAT helps reduce business costs and improves cash flow.

- Competitive Advantage: Being VAT registered can provide a competitive advantage over non-registered businesses, particularly if your customers are VAT registered themselves. VAT-registered customers can recover the VAT charged on your products or services, making your offerings more attractive compared to non-VAT registered competitors.

- Cross-border Trade: VAT registration is often required for businesses engaged in international trade. If you plan to import or export goods and services to or from the EU or other countries, having a VAT number simplifies the process and ensures compliance with relevant regulations.

- VAT Reporting and Record-Keeping: VAT registration necessitates maintaining accurate records of sales, purchases, and VAT payments. This can help improve financial management and provide a clearer picture of your business's financial health. It also ensures compliance with VAT reporting requirements, which helps avoid penalties and audits.

- Potential to Voluntarily Register: If your business turnover is below the mandatory VAT registration threshold, you can still choose to register voluntarily. This can be advantageous if your customers are predominantly VAT registered since you can reclaim VAT on your expenses while charging VAT on your sales, potentially resulting in a net VAT refund.

Disadvantages of VAT Registration

While VAT registration in the UK offers several advantages, it also comes with some potential disadvantages for businesses. Here are a few:

- Administrative Burden: VAT registration involves additional administrative tasks, including keeping detailed records, filing regular VAT returns, and complying with VAT regulations. This can increase the administrative workload for your business, especially if you are not habitual to managing VAT-related processes. VAT registration may require additional time, resources, and expertise to fulfil these obligations.

- Cash Flow Impact: VAT-registered businesses are required to charge VAT on their sales and collect it from their customers. This can have an impact on cash flow, particularly for businesses that primarily serve non-VAT registered customers. Collecting VAT means your customers will pay a higher price for your products or services, which may make your offerings less competitive and potentially reduce sales volume.

- Potential Complexity: VAT regulations and rules can be complex, and they often undergo changes. Staying up-to-date with these changes and ensuring compliance can be challenging, especially for small businesses without dedicated accounting or tax departments. Errors in VAT reporting or non-compliance can lead to penalties, fines, or audits by HMRC.

- Price Sensitivity: Some customers, particularly individuals or non-VAT registered businesses, may prefer to deal with suppliers who are not VAT registered. This is because non-VAT registered businesses may offer lower prices due to not having to charge VAT. As a VAT-registered business, you may encounter price sensitivity among certain customer segments, which could affect your competitiveness.

- VAT Inspections and Audits: VAT-registered businesses are subject to potential inspections and audits by HMRC to ensure compliance with VAT regulations. These inspections can be time-consuming and disruptive to normal business operations. If discrepancies or non-compliance issues are found during an audit, it can lead to penalties, fines, or additional tax liabilities.

- Impact on Small Businesses: VAT registration thresholds exist in the UK, and businesses below these thresholds are not required to register for VAT. For small businesses operating below these thresholds, registering for VAT voluntarily may not be financially beneficial. The additional costs and administrative burden associated with VAT registration might outweigh the advantages, particularly if the VAT input tax recovery is minimal.

One question we get asked a lot is:

If my business turnover exceeds £90,000 - do I need to pay VAT on all previous sales?

No. You must start paying the VAT from the date you register or when you reach the £90,000 threshold. You'll need to ensure you're tracking this, and can be done easily with accounting software like FreeAgent. We also include this for free with all of our packages.

When Do I Need to Pay VAT?

After registering, you'll need to file your return and pay VAT 1 month and 7 days after the end of your VAT quarter.

This is the most common VAT scheme for smaller businesses, with some that have an annual filing scheme (this is reserved for larger companies but can still mean monthly and quarterly filing). This is covered below but isn't a common requirement for most businesses in the UK.

With quarterly VAT filing, you'll need to ensure you're on top of your accounting admin at the end of each VAT quarter to ensure you file and pay the right amount.

You'll find that you'll fall into one of three groups for your VAT quarter end and filing period:

VAT Quarter Ends: Group 1

- January: covers the period 1st November to 31st January. You need to file your VAT return and pay by March 7th.

- April: covers the period 1st February to 30th April. You need to file your VAT return and pay by June 7th.

- July: covers the period 1st May to 31st July. You need to file your VAT return and pay by September 7th.

- October: covers the period 1st August to 31st October. You need to file your VAT return and pay by December 7th.

VAT Quarter: Group 2

- February: covers the period 1st December to 28th February. You need to file your VAT return and pay by April 7th.

- May: covers the period 1st March to 30th May. You need to file your VAT return and pay by July 7th.

- August: covers the period 1st June to 31st August. You need to file your VAT return and pay by October 7th.

- November: covers the period 1st September to 30th November. You need to file your VAT return and pay by January 7th.

VAT Quarter: Group 3

- March: covers the period 1st January to 31st March. You need to file your VAT return and pay by May 7th.

- June: covers the period 1st April to 30th June. You need to file your VAT return and pay by August 7th.

- September: covers the period 1st July to 30th September. You need to file your VAT return and pay by November 7th.

- December: covers the period 1st October to 31st December. You need to file your VAT return and pay by February 7th.

Legal Responsibilities After VAT Registration

Once you've registered for VAT, you'll need to:

- Keep Digital Records to Comply with Making Tax Digital (MTD)

- Issue VAT invoices

- Submit your VAT returns on time

1. Keep Digital Records to Comply with Making Tax Digital (MTD)

From April 2022, all VAT-registered businesses must comply with MTD, regardless of their annual turnover. HMRC will sign up all new VAT registered businesses to MTD automatically unless they are already exempt or have applied for exemption.

Under MTD, you're required to keep and maintain VAT records in “a compatible software that allows you to keep digital records and submit VAT Returns” or use “bridging software to connect non-compatible software (such as spreadsheets) to HMRC systems”. And if more than one software package is used, the packages must be linked digitally.

Records you need to keep digitally:

- Business name, address and VAT registration number

- Any VAT accounting schemes you use

- The VAT on goods and services you supply, for example, everything you sell, lease, transfer or hire out (supplies made)

- The VAT on goods and services you receive, for example, everything you buy, lease, rent or hire (supplies received)

- Adjustments you make to a return

- The ‘time of supply’ and ‘value of supply’ (value excluding VAT) for everything you buy and sell

- The rate of VAT charged on goods and services you supply

- Reverse charge transactions

- Total daily gross takings (if you use a retail scheme)

- Items you can reclaim VAT on if you use the Flat Rate Scheme

- Total sales and the VAT on those sales (if you trade in gold and use the Gold Accounting Scheme)

You're also required to keep digital copies of documents that cover multiple transactions made on behalf of your business by:

- Volunteers for charity fundraising

- Third-party businesses

- Employees for petty cash expenses

The records must be accurate, complete, and readable. You must keep records for at least 6 years (or 10 years if you used the VAT MOSS service)

Additional resources:

- HMRC's resource on VAT record keeping

- HMRC's Notice on digital record keeping (4.1), functional compatible software (4.2) and digital links (4.2.1)

2. Issue VAT Invoices

Depending on the type of VAT invoice you are issuing, you need to include the following:

*If items are charged at different VAT rates, you'll need to indicate the rates for each item.

3. Submit Your VAT Return

You must submit your VAT return online every quarter, even if you don't have VAT to pay or reclaim. How often you need to submit your VAT return may vary depending on the VAT scheme you choose, and we'll dive into this in further detail in the next section.

Under MTD, the deadlines for submitting your VAT returns remain the same. You're required to submit a VAT return and make payments a month and seven days after the end of a VAT period.

Here's an example: for a VAT period ending 31 March 2025, the due date for submission will be 7 May 2025. If you fail to submit your VAT return on time, you'll incur a penalty from HMRC.

What are My Options if I can’t Pay VAT?

Running into a cash flow issue is a common problem for small businesses. If you find yourself faced with a situation where you’re unable to pay VAT, these are steps you can take:

- Submit your VAT return: Don’t put this off, even if you can’t pay.

- Contact HMRC about setting up a Time to Pay (TTP) Arrangement: You might be able to set up a Time to Pay arrangement with HMRC, which allows you to pay your tax bill through a series of monthly instalments. Generally, TTP arrangements will not last beyond 12 months. In most instances, you must pay in full within three months.

- How to contact HMRC: The method you should use to contact HMRC will depend on whether you’ve received a payment demand, such as a tax bill or letter informing you about legal action that will be taken. If you’ve received a payment demand, you need to call up the HMRC office that sent out the letter. If you haven’t received a payment demand, you should call the Payment Support Service.

- Work out your options: Speak to your accountant to draw up a plan to meet your payments on time. You may look into small business financing options such as a line of credit or invoice factoring to help bridge your cash flow gap.

New VAT Penalties (2023 and beyond)

The new VAT penalty regime, which takes effect on January 1, 2023, represents a significant change from the previous default surcharge system. While some aspects of the new regime are an improvement, others could catch taxpayers and their agents unaware.

VAT Late Filing Penalties

One of the key differences is the points-based system for late filing penalties. Under this system, taxpayers receive one point for each VAT return they file late. Once their points reach a certain threshold, a fixed penalty of £200 will be charged. The threshold depends on how often the taxpayer files their VAT returns: four points for quarterly filers, five for monthly filers, and two for annual filers.

Once a taxpayer reaches their penalty threshold, each additional late VAT return will trigger a further £200 penalty. However, points can expire. If the taxpayer is below their penalty threshold, points will automatically expire after 24 months. If the taxpayer has reached their penalty threshold, points will only expire after a "period of compliance." This period requires all returns for a certain period to be filed on time and all outstanding VAT returns for the past 24 months to have been submitted. Once both conditions are met, the taxpayer's points total will be reset to zero. Importantly, unlike the default surcharge system, under the new regime, there is no connection between the amount of any late filing penalty and the VAT due on the return. This means that even repayment traders and taxpayers filing nil returns will be subject to late filing penalties for the first time.

VAT Late Payment Penalties

Late payment penalties are also changing. There will be two separate penalties based on how late payment is made. The first penalty will be 2% of the VAT unpaid on day 15, with a further 2% on day 30. After day 31, a second penalty will be charged daily based on an annual rate of 4% of the outstanding amount.

However, agreeing to a Time to Pay (TTP) arrangement with HMRC is treated in the same way as payment, with the penalty clock being "stopped" on the date of the original TTP application. If that TTP's terms are subsequently broken, it will be treated as if it never existed, and full penalties will be charged.

Under the new rules, paying or requesting a TTP within 15 days of the due date means no penalty will arise. Additionally, in the first year, the rules are in place. There will be a "period of familiarization," with HMRC not charging the first leg of the first penalty (i.e., the 2% at day 15) from January 1 until December 31, 2024. As a result, in that period, taxpayers can pay their VAT bills up to 30 days late without incurring a penalty (though interest will still be charged).

Interest

Another change is the interest rate for late payments. Late payment interest for VAT will be brought in line with other taxes, charged at the Bank of England base rate plus 2.5%. The existing repayment supplement will be withdrawn for VAT periods beginning on or after January 1, 2024. Instead, a much less generous repayment interest will be payable by HMRC at the Bank of England base rate minus 1%, with a minimum of 0.5%.

VAT Deregistration

VAT deregistration is the process of cancelling your VAT registration with HMRC. This can be done voluntarily or may be required under certain circumstances.

Voluntary Deregistration

- Turnover Below Threshold: You can voluntarily deregister for VAT if your taxable turnover falls below the VAT deregistration threshold, which is currently £88,000. This is useful if your business activities have decreased, and you no longer need to charge VAT.

- Ceasing to Trade: If you stop trading or close your business, you should deregister for VAT. This is because you no longer need to charge VAT or submit VAT returns.

Mandatory Deregistration

- Ceasing VAT-Taxable Supplies: You must deregister if you stop making VAT-taxable supplies. For example, if your business changes its activities and no longer sells goods or services that are subject to VAT.

- Joining a VAT Group: If your business becomes part of a VAT group, you must deregister individually since the group will handle VAT for all members.

Methods to Cancel VAT Registration

You may cancel your VAT registration online or by post.

1. Online

You’ll need your Government Gateway user ID and password to cancel online.

2. Cancel by Post

You’ll have to fill in the VAT7 form in full before printing it out and posting it to HMRC. The address for mailing is included in the form.

It’s best to have all the information you need to fill in the form on hand, as you won’t be able to save a half-completed form.

- Standard VAT Rate Scheme

- VAT Flat Rate Scheme

- Cash vs Invoice Accounting Scheme

- Annual Accounting Scheme

In addition to the standard rate scheme, small businesses are also eligible for other VAT schemes.

These are intended to minimise small businesses' administrative burden and cash flow issues.

1. Standard VAT Rate Scheme

Under the standard rate scheme, you'll reclaim VAT on each item you buy or sell, paying HMRC 20% of your invoices.

2. VAT Flat Rate Scheme

The flat rate scheme is available for small businesses and was introduced to simplify the VAT process.

Rather than pay the difference between the VAT you've charged your clients and the VAT on your purchases, you'll pay HMRC a fixed VAT rate.

To be eligible for the scheme, you must have an annual turnover of £150,000 or less (excluding VAT).

For further information, refer to our article on the flat rate scheme and limited cost trader.

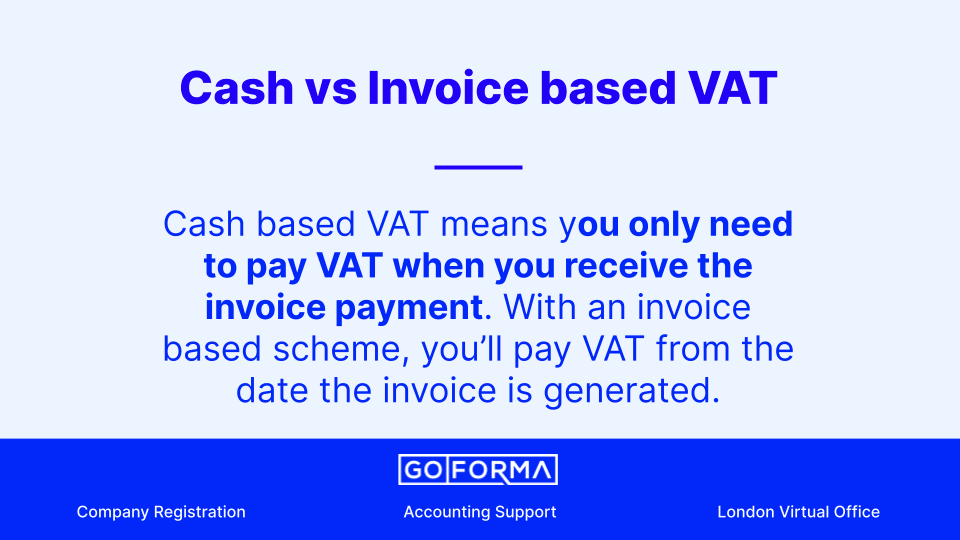

3. Cash vs Invoice Accounting Scheme

Under the cash accounting scheme, you account for VAT on the date you're paid rather than when you send out an invoice.

This is particularly helpful for small businesses dealing with late payers or cash flow concerns, as you'll pay VAT only after you've received payment.

The invoice scheme will mean that you pay VAT for the period when the invoice is generated, not when payment (cash) is received.

To be eligible for the cash accounting scheme, your estimated turnover for the following tax year shouldn't exceed £1.35m. Once you're on the scheme, you can use it until your turnover reaches £1.6m.

The cash-based scheme is the best scheme for new businesses.

4. Annual Accounting Scheme

With the annual accounting scheme, you'll make VAT payments on account. You can make either nine monthly payments or three quarterly payments (along with a balancing payment) and are required to complete one annual VAT return.

As with the cash accounting scheme, your estimated turnover for the following tax year shouldn't exceed £1.35m. And once you're on the scheme, you can use it until your turnover reaches £1.6m.

Your turnover, cash flow pattern and the type of clients or customers are just some of the factors you need to assess when choosing a VAT scheme.

Frequently Asked Questions on VAT Registration:

1. What does VAT stand for

VAT stands for Value Added Tax.

2. What is UK VAT registration

VAT registration in the UK is the process of registering for Value Added Tax with HMRC. It is mandatory for businesses that reach a certain turnover threshold (VAT threshold 2024 - £90,000). Registration involves submitting an application to HMRC, obtaining a unique VAT number, and displaying it on invoices. Registered businesses charge VAT on their sales, report it to HMRC through regular VAT returns, and keep records of their transactions. Different VAT schemes are available for simplified reporting. For accurate and up-to-date information, consult HMRC or a tax advisor.

3. Is VAT Registration mandatory in UK

Yes, VAT registration is mandatory in the UK for businesses that reach a certain turnover threshold. Currently, this threshold is set at £90,000 of taxable turnover in a 12-month period. Once a business exceeds this threshold, it is required to register for VAT with HMRC. Failure to do so can result in penalties and fines. However, businesses with a turnover below the threshold can still choose to voluntarily register for VAT if it suits their needs or if they want to take advantage of certain benefits or reclaim input tax.

4. How much does it cost to register for VAT

The cost of registering for VAT in the UK is generally free. There is no direct fee charged by HMRC for the registration process itself. However, it's important to note that registering for VAT may have financial implications for your business. Once registered, you will be required to charge VAT on your sales and submit regular VAT returns, which may involve additional administrative and accounting costs. Additionally, depending on your business activities and the nature of your transactions, there may be potential VAT liabilities or obligations to consider. It's recommended to consult with an accountant to understand the specific financial implications and obligations related to VAT registration for your business.

5. Where are UK VAT registration submitted

VAT registrations in the UK are typically submitted to Her Majesty's Revenue and Customs (HMRC). You have two options for submitting your VAT registration: Online: The preferred and most convenient method is to complete and submit the VAT registration application online through the HMRC website. This online service guides you through the application process, allowing you to enter the required information and upload any necessary documents.

Paper form: Alternatively, you can complete a paper form called VAT1 and mail it to HMRC. The form can be downloaded from the HMRC website, filled out manually, and sent to the designated address mentioned on the form. It's worth noting that the online application process is generally faster and more efficient, as it allows for immediate submission and reduces processing time. Regardless of the method chosen, it is important to ensure that the application is completed accurately and all necessary documents are provided to avoid any delays in the registration process.

6. What is the format of a VAT number

The UK VAT number consists of two letters followed by a series of numbers. The first two letters indicate the country code, which is usually "GB" for the United Kingdom. After the country code, the remaining part of the VAT number is a unique numeric identifier. For example, a UK VAT number might appear as GB123456789.

It's important to note that the length and specific format of a VAT number can vary based on certain factors, such as the type of business or special VAT schemes being used.

Additionally, businesses may have different VAT numbers for separate entities or branches. It's recommended to verify the correct format of a VAT number for your specific business by referring to the official documentation provided by HMRC or consulting with a tax advisor or accountant.

7. When Do I Pay VAT

You're required to submit a VAT return and make payments a month and seven days after the end of a VAT period.

8. Do You Pay VAT on the First £90,000

No, you do not need to pay VAT on your first £90,000 of taxable turnover. You must start paying the VAT from the date you register or when you reach the £90,000 threshold.

9. What is UK VAT Registration Threshold 2024

Currently, UK VAT threshold 2024 is £90,000 of taxable turnover in a 12-month period. This means that if a business's taxable turnover exceeds or is expected to exceed this threshold, it is required to register for VAT with HMRC.

10. My turnover is now below £90,000. Do I need to deregister for VAT?

You can stay VAT registered if your turnover is below the threshold, but you must cancel your registration within 30 days if you are no longer eligible. This could be because you stop trading, stop making taxable supplies, or join a VAT group. If your turnover is £88,000 or less, you can cancel your VAT registration online with HMRC. When you deregister, you might need to pay VAT to HMRC on any stocks and assets your business still holds.

Our Ultimate VAT guide walks through step by step what you need to know about registering for VAT, how to pay your VAT, your filing responsibilities and how to de-register for VAT.

- What is VAT

- When to register for VAT

- VAT rates

- Exempt/ Out of Scope VAT items

- VAT filing responsibilities

- De-registering for VAT

%20(1).webp)

Book a free 20 minute call with an accountant to talk though starting, registering or switching your company.

- Book a time online instantly

- Registering for VAT

- Self assessment

- Sole trader vs limited company

- Dividends and personal tax

- Registering your company